Our material matters

DETERMINING OUR MATERIAL MATTERS

Our external environment influences our ability to create value and achieve our strategic objectives , our relationships with our stakeholders and the risks and opportunities derived from these contexts.

We determine material matters by assessing these factors and aligning them to our strategy.

NB: Click the coloured heading on the blocks below to view further information

To ensure our strategy is both responsive and progressive, a robust understanding of our material matters is critical. We ensure our strategy incorporates matters that have the potential to influence our ability to create value in the short, medium and long term.

Our materiality assessments are based on matters identified as key risks and opportunities, as management continues to align its strategic approach with critical factors in our operating environment. All assessments are aligned to our strategic, financial, reporting, IT, compliance, reputational and operational risks.

The materiality determination process ranks our material matters based on relevance and impact on our ability to create value for our stakeholders.

Our enterprise risk management process evaluates the external environment and our stakeholders' expectations. We then outline the risks and opportunities that can considerably influence our ability to create value.

The Group considers the likelihood and the potential impact of the risks and opportunities within defined quantitative and qualitative parameters.

Our operating environment is dynamic and ever-changing. The Group's ability to monitor, assess and respond to the external environment and our material matters determines the Group's sustainability.

Quality stakeholder engagement is a key component of our ability to create value. Effective feedback and communication channels enable the Group to identify and address risks and opportunities. Stakeholder engagement also informs our material matters and our strategic response.

Executives review material matters annually to determine if there has been a change in the likelihood or magnitude of their effect on our business, or if new material matters have emerged.

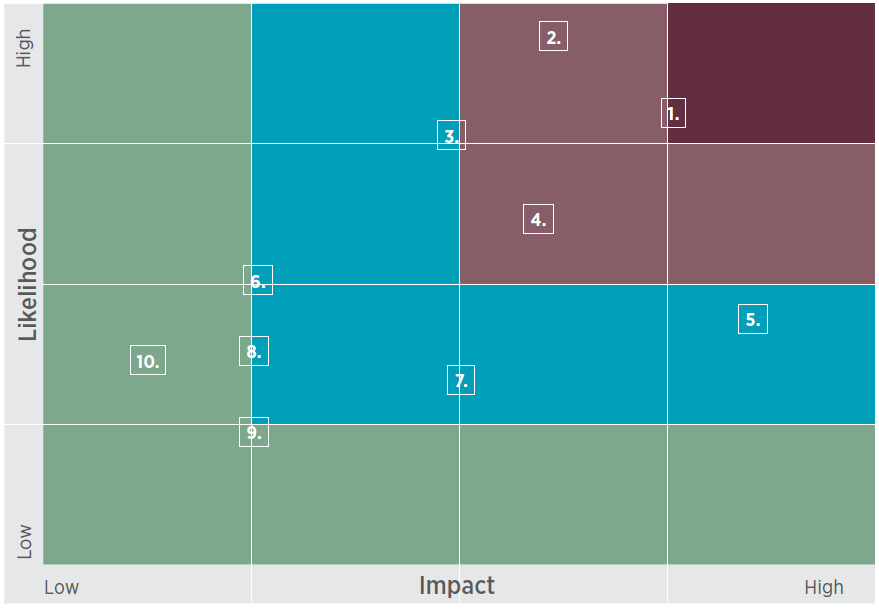

The heat map below depicts how these material matters were evaluated and prioritised based on their impact and likelihood.

MATERIALITY MATRIX

|

1. Escalating healthcare costs

2. Member retention for clients

3. COVID-19

4. Cybercrime and data security

5. IT dependency

6. Loss of critical skills

7. Technological innovation

8. Political and regulatory uncertainty

9. Transformation

10. FWA |

1. Escalating healthcare costs |

Trend  |

|

Why is it material to our business?

Rising healthcare costs make private medical insurance less affordable. This results in medical scheme membership losses and shifts to less costly scheme options which, in turn, impacts AfroCentric's revenue. |

Related risk

- Declining membership and the shift to less costly options threaten the sustainability of the private healthcare sector

|

Related opportunities

- Disruptive strategies to reduce inefficiencies

- Strategic purchasing of healthcare services throughout the value chain

- New acquisitions increase capacity to reduce healthcare costs

|

Our response

- Successful tariff negotiations to drive down pathology costs and hospital costs, and for more cost-effective products

- Implemented provider networks at reduced rates, e.g. hospital, day clinic, mental health and substance abuse facility networks and renal dialysis networks

- Management of supplier-induced demand using risk-sharing reimbursement models, in-hospital case managers, monitoring casualty conversion rates, and negotiating volume-based discounts

- FWA initiatives

- Initiated alternatives to hospitalisation, including encouraging in-rooms procedures, use of day clinics, step-down to subacute facilities and home-based care

- Implemented back and neck rehabilitation programmes to reduce costly back surgery

- Focused management of specific conditions to reduce the length of stay in hospital

|

Our response

- Implemented disruptive strategies to eliminate inefficiencies in the healthcare value chain

- Adopted technology and other initiatives to curtail pharmaceutical, specialist and hospital costs, including supplier agreements, e.g. for cardiac devices

- Collective bargaining

- Alternative reimbursement models with risk-sharing agreements

- Implement provider networks with a focus on cost containment, quality and outcomes

- Focus on provider profiling with remedial plans agreed and penalties for non-improvement

- In-hospital case managers onsite at outlier hospitals

|

Outlook

- Integrating acquisitions into the Group to achieve planned strategic value

- Maintaining the momentum of disruptive strategies

- Leveraging collective negotiation opportunities

- Focusing on value-based reimbursement models

|

Key stakeholders impacted

- Shareholders and investors

- Our clients – medical schemes

- Providers and suppliers of healthcare

- Regulators

|

Links to forward-looking strategy

- Technical and data analysis

- Pharmaceutical

- Cost efficiencies

- Value chain optimisation

- Disruptive models

- Primary care/health insurance

|

2. Member retention for clients |

Trend |

|

Why is it material to our business?

The heightened economic challenges faced by many due to the COVID-19 pandemic and its effects on businesses increased the need for affordable healthcare. |

Related risk

- Increased economic pressure may result in members opting out of their medical aid schemes

- Failure to help medical scheme clients retain their members by providing cost-effective service could result in losing clients

- Poor-quality service experienced by scheme members may also impact retention

|

Related opportunities

- Instilling a culture of quality client service

- Leveraging our integrated model to reduce costs to medical schemes while providing affordable, quality healthcare services

- Excellent service in times of crisis enhance customer loyalty

- Leveraging data analytics to identify ways of reducing member health risks and to better understand their needs

|

Our response

- Provided easy access to digital self-service on clients' websites and members' smartphones, including the addition of a WhatsApp functionality for enhanced client service

- Designed innovative scheme products and interventions to address declining affordability

- Enhanced our actuarial and analytics capability to understand our scheme lives and develop products and services to delight and assist members

- Partnered with various institutions, including Sanlam, to develop value-added products to assist with other elements of financial constraints for members

- Focused on improving call centre productivity

- Created specific teams to address retention for members, either directly or as service consultants for brokers

|

Our response

- ACT FIRST culture journey to instil a culture of quality healthcare

- Focused on providing innovative digital solutions to meet member needs and enhance efficiencies

|

Outlook

- Looking at further digital customer experience processes and channels, revised service model and more digital healthcare delivery models

- Saving money for our medical scheme members by reducing inefficiencies in the healthcare value chain and creating bespoke scheme options for specific member segments

|

Key stakeholders impacted

- Our clients – medical schemes

- Scheme members

- AfroCentric employees

- Brokers

|

Links to forward-looking strategy

- Technical and data analysis

- Client experience and membership growth

- Cost efficiencies

- Value chain optimisation

- Disruptive models

- Primary care/health insurance

|

3. COVID-19 |

Trend (new matter) |

|

Why is it material to our business?

Traditional administration and managed care businesses rely on revenues generated from the membership of client medical schemes. In the current context, there is a risk of reduced revenue due to potential membership losses as a consequence of the economic downturn. |

Related risk

- Medical schemes face additional expenditure due to the cost of COVID-19 testing, personal protective equipment (PPE) and hospitalisation

- Scheme reserves were initially under pressure due to poor investment returns. Although markets have subsequently improved, returns from medical scheme investments will likely remain volatile

- Although it is difficult to accurately quantify the impact of COVID-19 on client medical scheme membership, it is likely that the economic consequences of job losses and upward pressure on contributions could result in membership terminations and buy-downs

- In addition, remaining membership profiles are likely to deteriorate, which will place further pressure on contributions

|

Related opportunities

- The COVID-19 pandemic will likely change the trajectory for healthcare delivery in South Africa, and AfroCentric is well positioned to capitalise on these opportunities

- Specific opportunities include:

- Increasing the use of technology to enable social distancing, for example, virtual consultations

- Building public-private partnerships as the state sector capacity is overwhelmed by the pandemic

- Fast-tracking opportunities to build on managed care interventions that channel beneficiaries to day surgery facilities and alternatives to hospitalisation

- Creating opportunities to increase the utilisation of AfroCentric companies in the healthcare value chain to lower the cost of care while maintaining or improving quality

- Opportunities are created in the corporate workspace, especially as employees return to work

|

Our response

- Medscheme played a vital role in negotiating the pathology tariff for the COVID-19 PCR test, which resulted in a substantial price reduction

- Implementing risk management interventions, including developing digital solutions to ensure COVID-19 testing is funded as per the National Institute for Communicable Diseases (NICD) guidelines

- Ongoing negotiations with hospital groups for PPE to optimise the additional costs these incur

- Implementing a COVID-19-specific rapid response call centre

- Working with clients on new benefit design options for 2021 that will enable more affordable contributions while still providing access to quality healthcare

|

Our response

- Launching a digital platform to enable virtual consultations

- Using the digital platform to assist members with COVID-19 screening

- Engagements with the provincial government on providing administrative support for public patients being admitted to private hospitals contracted to the NDoH

- Managed care solutions to channel members to day surgery and alternatives to hospitalisation are being developed

- Disease management is being re-engineered to drive clinical outcomes

- Evolving new solutions that incorporate Group companies in the healthcare value chain that will lower the cost of healthcare

- AfroCentric Integrated Corporate Solutions and Wellness Odyssey are providing COVID-19 screening, occupational health and employee assistance programme solutions to corporate pay points of client medical schemes

|

Outlook

While the COVID-19 pandemic has produced many challenges for the healthcare sector, it also created several opportunities threatening to disrupt the current healthcare delivery model. This changes the playing field in the private healthcare sector and AfroCentric, as the largest diversified healthcare company in Southern Africa, is well positioned to leverage these opportunities. |

Key stakeholders impacted - AfroCentric employees

- Our clients – medical schemes

- Government

- Regulators

- Providers and suppliers of healthcare

|

Links to forward-looking strategy

- Technical and data analysis

- Pharmaceutical

- Cost efficiencies

- Value chain optimisation

- Disruptive models

- Primary care/health insurance

|

4. Cybercrime and data security |

Trend |

|

Why is it material to our business?

With advanced technology comes the increased threat of cybercrime. Inadequate investment in cybercrime detection and prevention makes businesses vulnerable to cyberattacks. |

Related risk

- Cybersecurity breaches expose our intellectual property and client data to the risk of leaks or compromise. This could damage our client relationships and reputation

|

Related opportunities

- Advanced threat analytics technology strengthens the security of our systems

- Cybersecurity strategy review ensures continuous updating of systems, including web application firewalls

|

Our response

- Applied a proactive approach with improved evaluation and analysis of cybercrime and data security risks

- Enabled faster detection and response to rapidly evolving cyber threats

- Implementing Privilege Account Manager which is a supervisory tool to track activities and changes by privileged users

|

Our response

- Reviewed our cybersecurity strategy

|

Outlook

- Continuously investing in identification, detection and prevention technologies to mitigate risk and keep dwell time below 60 days

- Ensuring ongoing user awareness of cyber threats and vulnerabilities

|

Key stakeholders impacted

- Trade suppliers

- Our clients – medical schemes

- AfroCentric employees

|

Links to forward-looking strategy

- Technical and data analysis

- Client experience and membership growth

|

5. IT dependency |

Trend |

|

Why is it material to our business?

Our IT architecture forms the core of our operations. Stable IT systems and adopting digital technology support operational efficiency and customer service during a period of business growth and market consolidation. |

Related risk

- IT system instability exposes the Group to the risk of business interruption, while failure to respond to disruptive technologies may impact our competitive advantages

|

Related opportunities

- Adopting artificial intelligence (AI) and RPA

- Enterprise architecture and IT

- Technology operating model

|

Our response

- Establish an architecture oversight and governance structure to improve efficiency and service

|

Our response

- Reviewed our digital strategy to strengthen innovation focus

|

Outlook

- Continuously improving IT architecture is expected to improve service and reduce costs

|

Key stakeholders impacted

- AfroCentric employees

- Our clients – medical schemes

- Trade suppliers

|

Links to forward-looking strategy

- Technical and data analysis

- Client experience and membership growth

- Disruptive models

|

6. Loss of critical skills |

Trend |

|

Why is it material to our business?

AfroCentric competes for skilled and experienced employees in the global and local healthcare sector. Retention of intellectual capital, particularly of actuarial, IT and medical specialists, is imperative. |

Related risk

- A shortage of critical skills in the domestic healthcare sector necessitates retaining existing skills and attracting new skills

|

Related opportunities

- Succession planning and short-term and long-term incentives attract and retain critical skills

- Training and development support retention plans

|

Our response

- Building an external pipeline of critical talent and an internal pipeline of successors for critical roles

- Implemented a leadership competency model to create common leadership behaviour that promotes employee engagement

- Implemented a scarce skills retention strategy

|

Our response

- Undertook numerous training and development initiatives

- Developed internal talent pipelines for critical roles in progress

- Reviewed short-term and long-term incentives

|

Outlook

- Mitigating risk of losing critical skills by implementing retention and succession strategies

- Implementing a culture shift programme to help employees adapt to a culture of innovation

|

Key stakeholders impacted

|

Links to forward-looking strategy

|

7. Technological innovation |

Trend |

|

Why is it material to our business?

Technological innovation enhances cost-efficiency and enables the Group to remain relevant to clients. In a rapidly evolving digital environment, increased digitisation improves client experience and is a competitive advantage. Furthermore, COVID-19 and the resultant lockdown amplified the need for digital solutions and accelerated the uptake of digital means of engaging with and delivering services to clients and scheme members. |

Related risk

- Not staying abreast of technological advances limits the Group's ability to implement its strategy effectively

|

Related opportunities

- Leveraging current digital capabilities to reduce cost, improve client experience and drive member growth and retention with value-added products and services

|

Our response

- Adopted a Group digital strategy

- Expanded RPA to one million transactions

- Implemented an innovative, new benefit design for scheme members and upgraded schemes' digital self-service facilities

- Implemented electronic health record systems for high-risk patients

|

Our response

- Currently leveraging digital capabilities to the value of R35 million that improve client experience and drive member growth and retention with value-added products and services

|

Outlook

- Continue the rapid migration to digital technologies driven by the pandemic

- Continue reducing healthcare costs and improving client experience

- Identifying and implementing new products and services to maximise growth objectives

|

Key stakeholders impacted

- Medical schemes

- Medical scheme members

- Brokers

- Employees

|

Links to forward-looking strategy

- Technical and data analysis

- Client experience and membership growth

- Cost efficiencies

- Disruptive models

|

8. Technological innovation |

Trend |

|

Why is it material to our business?

The healthcare sector is experiencing policy uncertainty related to the NHI bill and other healthcare legislation. Challenging economic conditions, exacerbated by political uncertainty, contribute to a decline in medical scheme memberships. |

Related risk

- The draft NHI and Medical Scheme Amendment (MSA) bills propose changes to the roles of healthcare businesses and will impact the future of the private healthcare sector

- Failure to comply with legislative requirements can harm financial, reputational or business sustainability

- COVID-19 and the resultant lockdown contributed to a potential negative impact on the business and its revenue streams. For example, client medical schemes may experience a decline in membership numbers which will impact them financially due to a decline in contributions and healthcare utilisation costs

|

Related opportunities

- Position as a diversified healthcare partner in the delivery of healthcare for all in South Africa

- Participate in public-private partnerships to demonstrate this capacity

|

Our response

- Diversified revenue sources and service and product offerings

- Partnered with government to drive universal healthcare agenda

- Promoted transformation

- Engagement with government via Business Unity South Africa and Board of Healthcare Funders to pledge support, offer solutions and identify opportunities for private sector involvement in the COVID-19 pandemic response

|

Our response

- Leverage existing contractual arrangements with National and Provincial Departments of Health (DoH). For example, CCMDD to roll out COVID-19 pandemic responses

- Leverage existing relationships with private hospital groups to design and implement interventions to support National and Provincial DoH in dealing with projected increased numbers of COVID-19 related infections

|

Outlook

- Continue positioning AfroCentric as a diversified healthcare partner in the delivery of healthcare for all in South Africa

|

Key stakeholders impacted

- AfroCentric businesses

- AfroCentric employees

- Our clients – medical schemes

- Government – national and provincial

- Regulators

|

Links to forward-looking strategy

- Cost efficiencies

- Value chain optimisation

|

9. Transformation |

Trend |

|

Why is it material to our business?

AfroCentric is an empowered business committed to South Africa's transformation agenda. Transformation is a strategic objective, and we aim to comply with the B-BBEE codes and other relevant legislation. |

Related risk

- Poor transformation performance impacts the Group's ability to secure new work and would hinder the Group's ability to have a positive impact on its operating communities

- There is a potential loss of business with no B-BBEE certificate

- With government business, dependent on the size of the tender, B-BBEE accounts for 10% to 20% of the price differential

- The B-BBEE Act makes implementation compulsory for the state and its associated enterprises

- Section 10 of the B-BBEE Act requires government to consider your B-BBEE status when granting licences and concessions

- The B-BBEE Act makes it compulsory for JSE-listed companies to comply and report to the B-BBEE Commission

|

Related opportunities

- Our level 1 B-BBEE status favourably positions the Group to win tenders in the public and private sectors

- Our B-BBEE status demonstrates our commitment to transformation

- Opportunity to empower staff through retention and skills development and suppliers and small business through preferential procurement and enterprise and supplier development

- Opportunity to impact the greater community positively through SED

- Companies use our B-BBEE certificate to make their purchasing decisions

|

Our response

- Improved AfroCentric's black ownership to 57%

- Integrated businesses with B-BBEE requirements

- Consistently applied preferential procurement practices across the Group

- Improved reporting and measurement

- Significant improvements in the integration of business processes with B-BBEE requirements

- Formulated Group policies and procedures with regard to the five B-BBEE elements in place

- Formulated and implemented preferential procurement practices that align procurement to B-BBEE imperatives in a consistent manner across the Group has improved

- Made substantial improvements to the AfroCentric Health (RF) Proprietary Limited (AHL) B-BBEE reporting and monitoring framework. This ensured alignment and consistency in reporting and enabled measurement of performance and the ultimate impact of B-BBEE activities

|

Our response

- Maintained our B-BBEE status at level 1 (this status is valid from 30 November 2019 to 29 November 2020)

- B-BBEE level result is aligned with the transformation and empowerment requirements as specified by current and prospective clients

- There are increased partnerships within the Group to achieve B-BBEE priority objectives, emphasising skills development, enterprise and supplier development and ownership

- Facilitate Black Economic Empowerment (BEE) through targeted interventions to achieve more inclusive growth

- Create an environment enabling transformational development in an equitable and socially responsible manner

- Provide trend and other in-depth analysis in easy to read formats to measure the transformation gains across the Group

- Extend relationships with critical stakeholders for the betterment of the organisation in relation to B-BBEE

- Promote a professional, ethical, dynamic competitive and customer-focused environment with regard to BEE

- Ensure all stakeholders are aware of the purpose of the B-BBEE Act

- Increase visibility by providing activities, education and information and resources

|

Outlook

- Maintaining level 1 B-BBEE status

- Improving performance in skills development and employment equity

|

Key stakeholders impacted

- Employees

- Our clients – medical schemes

- Trade suppliers

|

Links to forward-looking strategy

|

10. Fraud, waste and abuse (FWA) |

Trend |

|

Why is it material to our business?

Losses are incurred, and healthcare costs escalate when third parties defraud our client schemes and/or our employees through unauthorised, fraudulent and wasteful activities. |

Related risk

- Fraudulent and wasteful claims severely impact the financial sustainability of medical schemes; contributing to increased membership costs, which may result in membership losses and solvency challenges

|

Related opportunities

- FWA management and data analysis by forensics enable quantification, reduction and, in some cases, recovery of funds

- More importantly, it creates the necessary awareness and oversight in terms of claims monitoring and payment

- Intensive intervention improves billing patterns and claims behaviour

|

Our response

- Reviewed and enhanced FWA processes, communication templates and strategies

- Introduced additional quality standards for provider communications

- Enhanced and improved analytics and reporting capabilities on the forensic system

- Claims behaviour monitoring

- Increased intelligence and industry collaboration

|

Our response

- Leverage benefits presented by the growing consortium of schemes that we provide forensic services to

- Continuous and enhanced FWA responses

- Communication, awareness and training for our stakeholders

- Changing billing behaviour and ensuring rehabilitation

- Highest per member recovery rate in the industry

- Maximising value to the client by improving the schemes' financial health and stability

- Market differentiator for current and new clients

- Effective FWA programme that adds value to the healthcare administration and managed care strategy by continuously highlighting emerging FWA trends/patterns and recommended mitigations

|

Outlook

- Identifying and addressing process gaps in FWA management

- Staying abreast with latest FWA trends and modus operandi

- Continuously investing in technology resources and innovations to ensure only valid and legitimate claims are paid

- Recovery of funds obtained through FWA

|

Key stakeholders impacted

- Our clients – medical schemes

- Medical scheme members

- Potential clients

- Employees

- Group subsidiaries

|

Links to forward-looking strategy

- Technical and data analysis

- Client experience and membership growth

|

|

|

|

No movement |

|

|

Moved up |

|

|

Moved down |