CFO’S REVIEW

Aligning shareholders earnings and operating profit growth by maximising organic growth opportunities.

The 2021 Financial year will probably in future be known as the most uncertain time to do business in the world due to the changing trading conditions abroad and in South Africa. The Group was faced with significant opportunities in patients demanding medication more promptly out of fear for logistical backlogs and the need for preventative medication in the form of vitamins, whilst the reduction of the employed workforce in South Africa could have a significant impact on medical scheme membership. Planning for financial certainty and agility to react to these opportunities, I believe this has been the winning recipe for AfroCentric in recording continuous growth in its earnings base to shareholders.

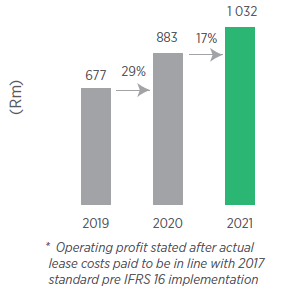

Operating profit*

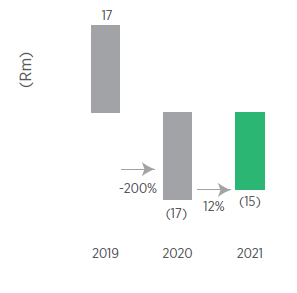

Net cash finance

income/(cost)

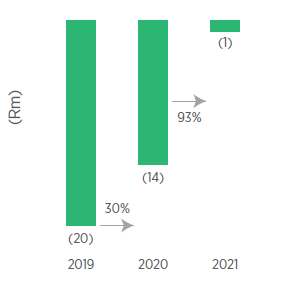

Depreciation/amortisation

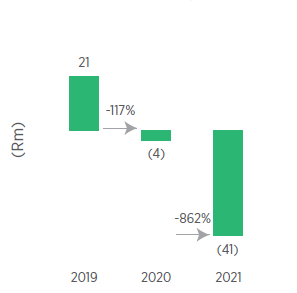

IFRS 16 (leases) net effect

Other (impairments, share

based payment)

Profit before tax

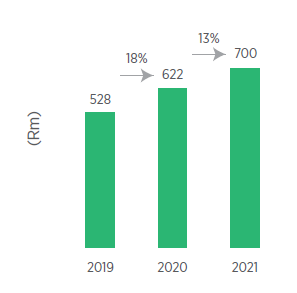

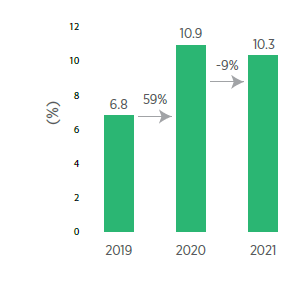

During the 2021 financial year, AfroCentric achieved its goal of exceeding a R1 billion earnings before interest, taxes, depreciation, and amortisation (EBITDA) level which was narrowly missed in 2020. As a Group that is still growing and diversifying its product offering in the healthcare market, we are delighted to finally achieve this milestone. While the Group achieved significant growth in its operating profit, this has not filtered down to profit before tax, driven largely by increased depreciation and amortisation in the 2021 financial period. The Group's strategy of diversifying its product offering by investing in the value chain of healthcare services have been the main reason for increased amortisation over the past few years with significant acquisitions like Activo Health in 2019 and Denis in 2020. The investment in our internally developed administration system during 2015 to 2018 with final implementation in the 2019 year have also contributed to enhanced amortisation.

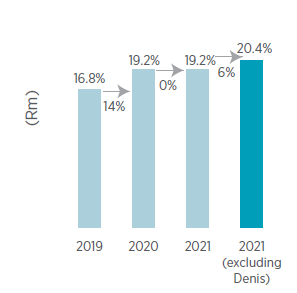

The benefits of the above acquisitions have resulted in growth in the pharmaceutical cluster in excess of 30% whilst the efficiency in which the Medscheme South Africa business is managing its clients are improving with net profit growth of 11% if the Denis acquisition profits are excluded in 2021 (see notes below).

During the year, the Group deployed various digital initiatives where members started interacting directly on a software application or via WhatsApp and even conducting virtual consultations with a general practitioner. These trends and fast growing technology and systems are replacing older client interfacing modules, this has resulted in the Group impairing and derecognising items that are no longer being used. The net impairment impact in 2021 mainly relate to older digital development work that has been replaced.

The Group foresees that we will make similar impairments in the medium to long term as technological advances make software processes more agile and module based and indirectly replaces older development code.

Profit before tax continues to grow in double digits which is aligned to our long term goal of extracting more value out of the healthcare market in South Africa. Notably the strategies and growth rates do vary based on the main healthcare sectors our business units are competing in which is further analysed below.

Healthcare Services Financial Performance

The traditional medical scheme administration and managed care business that mainly consists of Medscheme have consistently been exceeding expectations in operating profit due to the difficult market conditions they operate in. With limited growth in insured lives in South Africa, the Medscheme membership has been able to retain its membership base consistently in the four largest schemes we manage being, Bonitas, Fedhealth, Polmed and GEMS. In the past twelve months we have recorded net growth in both Bonitas and GEMS which indicates the stickiness the public still have for private healthcare benefits and that the South African middle class have not been impacted too harshly by the reduction in employment.

The focus in Medscheme, being the primary subsidiary of the Group responsible for medical scheme administration, has been to build systems and processes of excellence. These projects where different teams compete on a "Single Service Measure" enabled competition in the business units that resulted in improved customer service and turnaround time of transactions. The rollout of other digital enhancements in the member applications, WhatsApp communication and chatbots have also driven more customer volumes to a digital platform that is 24/7 enabled and reliable. An improved hospital approval system linked to the major hospital groups in South Africa will further enhance the turnaround time, case management and payment cycles of hospital claims and thereby reducing transaction costs for this particular service.

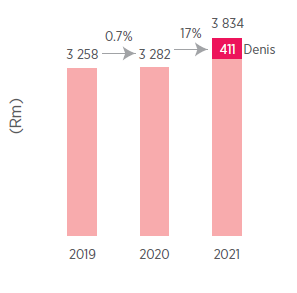

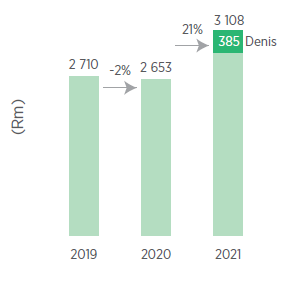

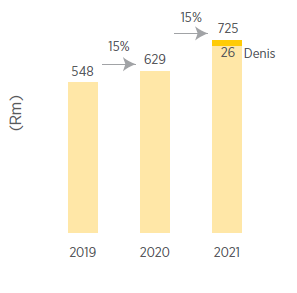

The Medscheme team together with their IT counterparts have continued to deliver sterling results in this mature business unit by reducing costs and improving efficiencies. If the effect of Denis is excluded, the services business were able to increase revenue by 4.3% whilst only increasing operating costs by 2.6%. This resulted in the double digit increase in operating profit of 11% if Denis is excluded.

Revenue

Operating costs

Operating profit

Operating margin

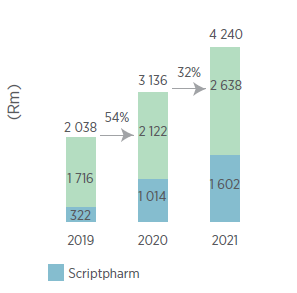

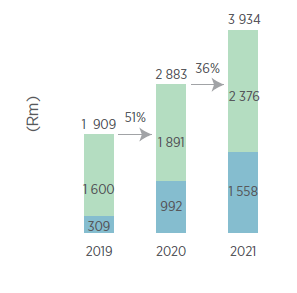

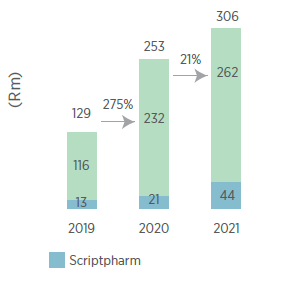

Healthcare Retail Financial Performance (Pharmaceutical)

The Pharmaceutical division has continued its expected growth trajectory during 2021 and was specifically supported by the

Revenue

Operating costs

Operating profit

Operating margin

(excluding Scriptpharm)

Pharmacy Direct continued its script growth during the year and consistently delivered in excess of 1 million chronic scripts to public patients, whilst the private medical scheme script count exceeds 170 000 per month. The improved operating profit was however not only due to increased volumes but as a result of improved cost efficiencies in the packing and distribution of the medication. In the latter part of the year, a new robotics system has been installed in the private side of the business and will yield significant return in the 2022 financial year.

Capital management

The Group has experienced some significant turnarounds in its balance sheet since 2015 by first having excessive cash on hand with the subscription of shares sale to Sanlam and the issue of additional shares that funded the initial pharmaceutical assets. These new businesses compared to a stable cash generating medical scheme administration business have required the management team to look at different ways in which growth can be supported. For this very reason the Group has continued to rather fund acquisitions through debt since 2019, as no gearing was in place then, and the continued working capital needs are being monitored and reviewed on a weekly basis with targets set for each unique business.

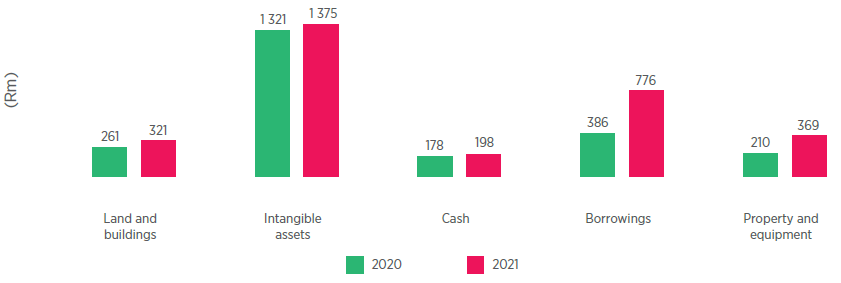

These trends of acquisitive growth are the main drivers of significant movements in our statement of financial position at 30 June 2021 as set out below.

Optimising our Capital Structure whilst absorbing new acquisitive opportunities is a balancing act.

Significant movements

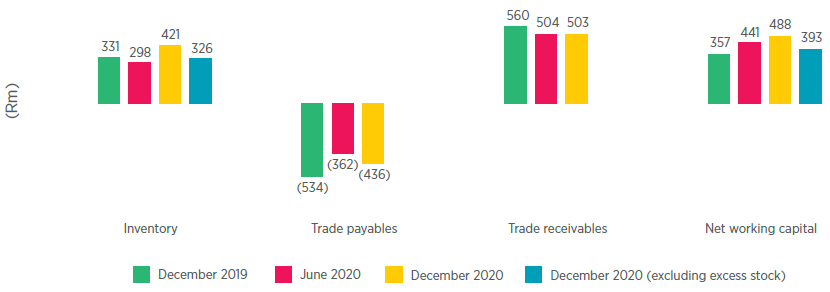

Working capital

The Denis acquisition was the main contributor to some asset growth in the form of a new building that was included as well as IT and office assets.

The objective of matching capital expenditure incurred with regards to IT development and matching it with amortisation is starting to pay off and therefore the increase in intangible assets is most notably the customer relations stemming from the Denis acquisition's purchase price allocation.

The Group continues to optimally manage with an approximate R200 million cash float which is used for short term payments and working capital needs.

Working capital as depicted above has grown, especially inventory, but if the excess inventory as a result of new product launches (slow moving in first two years of launch) is excluded, the inventory levels have actually been managed down from prior years and with cognizance of growth experienced.

In conclusion

AfroCentric has a proven track record of acquiring new businesses and integrating their products in a seamless way to provide customers with a continuous experience in healthcare services and products. This philosophy will continue and whilst we are probably nearing the end of a period of acquisitions, the organic growth opportunities will now be focused upon for further expansion.

The optimal capital structure of equity, debt and working capital balanced by a reasonable dividend policy is continuously being reviewed to ensure the sustainability of earnings of the Group and returns for our shareholders.

I would like to thank the Group Finance team for their dedicated hard work and commitment to consistently being innovative in the support to the group from a financial and commercial level which we reap the benefits of in the results shown above.

Hannes Boonzaaier

Group CFO